) or https:// means you’ve safely connected to the .gov website. Share sensitive information only on official, secure websites.

) or https:// means you’ve safely connected to the .gov website. Share sensitive information only on official, secure websites.FAQ

The following answers provide a combination of general and some technical information. This information should only be considered as a starting point due to the complexity of each situation. This content does not have the force and effect of law, rule or regulation.

Employer Registration & Taxes

How do I change my Employer Registration address?

To change your address you must sign into E-gov and scroll down to Employer Registration/Account Status and click on Mailing Address. And follow the prompts. Click here to begin.

When is an individual considered an employee?

An Alabama worker is an employee if an employee/employer relationship exists between the business and the worker. This means if a business has the “right of control” over the worker—whether or not they actually exercise the right—the worker is an employee. Alabama law further provides that we use the common law factors to assist us in making determinations. Additionally, you may click here for some examples of independent contractors versus employees. If you have further questions, you may contact your local field tax representative.

How do you meet liability for Alabama State UC Taxes?

The Alabama UC law provides that, except for certain non-profit organizations and government entities, an employer becomes subject for taxes when any one of the following conditions are met:

- Non-Farm Business Employers

- When the employer has had in employment one or more workers on some day in 20 or more different weeks, whether or not consecutive, during the current or preceding calendar year.

- Has paid wages of $1,500 or more in any calendar quarter during the current or preceding calendar year.

- Household Domestic Employers

- Domestic employers become subject when the employer pays domestic workers in a private household, college club, fraternity or sorority house a total of $1,000 or more in cash wages in any calendar quarter during the current or preceding calendar year.

- Agricultural Employers

- When the employer has had in employment ten or more agricultural workers in 20 or more different weeks during the current or preceding calendar year or has paid a total of $20,000 in wages to agricultural workers during any calendar quarter of the current or preceding calendar year.

For additional information on establishing liability for Alabama Unemployment Taxes, contact the Status Unit at 334-954-4730 or status@workforce.alabama.gov.

What constitutes a successor employer?

An employer becomes subject by:

- Acquiring the trade or business, organization, or substantially all the assets of another employer which at the time of such acquisition was an employer subject to Alabama Unemployment Tax.

- Acquiring a segregable part of the organization, trade or business of another employer which was at the time of acquisition an employer subject to Alabama Unemployment taxes, provided that the segregable part would itself have been an employing unit subject to Alabama Unemployment Tax had it represented the entire business of the predecessor.

For additional information regarding successor employers, contact the Status Unit at 334-954-4730 or status@workforce.alabama.gov.

Are religious organizations liable for Unemployment Taxes?

The Alabama UC law provides that services performed in the employ of a church or convention or association of churches—or an organization that is operated primarily for religious purposes and which is operated, supervised, controlled or principally supported by a church, convention or association of churches—shall not be considered covered employment. For more information on religious organizations contact the Status Unit at 334-954-4730 or status@workforce.alabama.gov.

Are non-profit organizations exempt from Alabama Unemployment Tax?

Non-profit organizations are liable for Alabama Unemployment Tax unless they are exempt from income tax under section 501(a) of the Internal Revenue Code and are classified as a Section 501(c)(3) exemption organization.

Non-profit organizations that are classified under Section 501(c)(3) become liable for Alabama Unemployment Taxes only after they have had four or more individuals in employment in each of 20 different weeks within either the current or preceding calendar year. For additional information on non-profit organizations, contact the Status Unit at 334-954-4730 or status@workforce.alabama.gov.

How does my business register as a new employer?

Once wages have been paid for work performed in Alabama, you may apply for a new number with eGov. If the system advises you to submit the paper application, please do so.

Tax Rates

How do I get my new tax rate notice?

You may download your tax rate notice by logging into eGov, provided your company is not a new company with a 2.70% rate (initial rate). Employers who have a 2.70% rate will be able to download a computer generated tax rate notice once their individualized tax rate is determined for them.

What is the new account rate?

Employers newly liable under the Alabama UC law pay tax at the rate of 2.70% on the first $8,000 of wages for each employee. Subsequent rates are determined by Experience Rating. You may contact the Experience Rating Section at 334-954-4741 if you have other questions.

May a tax rate transfer from an existing employer to a new employer?

A new employer that acquires the organization, trade or business of another liable employer (the predecessor) is assigned the experience (benefit charges and taxable payroll) of the predecessor. The predecessor’s experience is used to determine the successor’s tax rate. If proper notification and wage transcripts are provided to the Alabama Department of Workforce within the time prescribed by the Alabama UC law, the new employer may be entitled to a rate based on partial acquisition of the predecessor. You may contact the Experience Rating Section at 334-954-4741 if you have other questions.

May an employer earn a tax rate based upon its record of unemployment experience?

An employer which has operated a sufficient period of time to qualify for experience rating earns a tax rate based upon the employer’s own experience (benefit charges and taxable payroll), modified by statewide experience (schedule and shared cost). Inclusive of the 0.06% Employment Security Enhancement Assessment (ESA), an Employer’s rate can vary from 0.20% to 6.80% depending on the one of four rate schedules in effect, plus any applicable shared cost. Refer to the tax rate calculation information for defined tax terms, like tax rate schedule, shared cost and ESA.

You may contact the Experience Rating Section at 334-954-4741 if you have other questions.

How is my annual tax rate calculated if the rate is based on experience?

The rate is computed using the three most recent complete fiscal years of benefit charges and taxable payroll. A fiscal year begins July 1 and ends the following June 30.

Benefit charges (Item 9 on the Tax Rate Notice, Form UC-216) are costs for actual benefits paid to former employee(s). Taxable payrolls (Item 10) include taxable wages upon which taxes have been paid by the preceding July 31. Your benefit ratio (Item 11) is determined by dividing total benefit charges (Item 12) by total taxable payroll (Item 13) for the three most recent complete fiscal years.

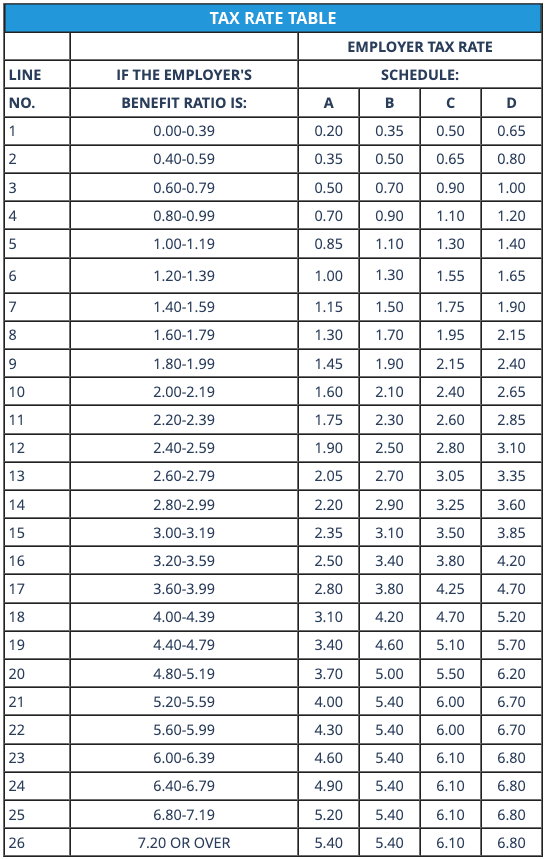

With knowledge of your benefit ratio (Item 11) and statewide schedule (Item 3), you can verify the computed rate (Item 5) and tax rate (Item 6) in the Tax Rate Table. An excerpt of the Tax Rate Table contained in Section 25-4-54(f) of the Alabama Unemployment Compensation (UC) Law is listed below.

The statewide schedule (Item 3) and shared cost (Item 4) are determined in accordance with 1989 amendment to the Alabama Unemployment Compensation Law. The amendment contains four rate schedules: A, B, C, and D. The applicable schedule is determined yearly by a formula that looks at the relationship of the Unemployment Compensations Trust Fund’s balance to the desired level of the Fund. Shared cost (Item 4) is determined yearly and is defined as cost that cannot be assigned to a specific employer. Shared cost (Item 4) is added to the computed rate (Item 5) to determine the tax rate (Item 6). Employment Security Enhancement, or ESA (Item 7), monies are deposited to the Employment Security Enhancement Fund in the State Treasury and used to assist unemployed claimants in obtaining employment.

To verify the tax rate (Item 6), find the line and benefit ratio range which corresponds with your benefit ratio (Item 11) on the Tax Rate Notice. Follow across to the applicable tax rate schedule (Item 3) given below to determine your rate. If your benefit ratio is 0.37%, your rate under Schedule C is 0.50%. All rates must be reduced by 0.06% ESA except 5.40%. After the 0.06% reduction, the rate will agree with the computed rate (Item 5) on the Tax Rate Notice. The computed rate would be 0.44% for this example. Add shared cost (Item 4) to the computed rate (Item 5) to determine the tax rate (Item 6) on the Tax Rate Notice. Your rate (Item 6) and ESA (Item 7) may be combined to determine your total rate at which payment is computed quarterly.

To view general information about the tax rate system, you may download the current publication of the “Employer Handbook” from our website. The complete tax rate schedule, Tax Rate Table and shared cost from the UC law may be viewed online. You may contact the Experience Rating Section at 334-954-4741 if you have more questions.

How do benefit charges for unemployment compensation claims affect an employer’s tax rating account?

When an individual files a claim for benefits, two determinations are made.

The first is a monetary determination of the amount of benefits the claimant may receive based on his/her wages paid in a specified time period (base period). The second is a non monetary determination that considers the claimant’s eligibility for benefits and reason for separation from employment. Both determinations affect the charging of the employer’s account.

The gross wages paid to a claimant by all employers in the base period are used in determining a claimant’s weekly benefit amount (WBA) and maximum benefit amount (MBA). An employer’s charging for benefits is based on the following elements:

- Base Period Gross Wages Paid by the Employer: The base period is defined in Alabama’s UC law as the first four of the last five completed calendar quarters prior to the filing of the claim, and is used to establish eligibility for benefits.

- Cost Ratio (Percentage): If a claimant has only one employer in the base period, that employer’s account would be charged for 100% of the cost for benefits paid and chargeable. If the claimant had two or more employers during the base period, each employer’s liability would be determined by its percentage of the total gross wages paid by all base period employers.

The percentage multiplied by the total amount of benefits ultimately received by the claimant while unemployed equals the employer’s benefit charges.

After the end of each quarter, an employer receiving benefit charges during the quarter is mailed a statement of the benefit charges. Benefits charged to the employer’s account may increase the employer’ tax rate and result in higher tax payments that will enable the Trust Fund to recover the benefits paid over a three year period. You may contact the Experience Rating Section at the telephone number and address shown at the end of this section if you have other questions.

Are there non-charges and credits?

Provisions of the Alabama UC law allow tax rated employers to receive relief from benefit charges and immediate credits for overpaid benefits. In order to receive consideration of non-charging, the employer must respond timely to the separation, determination and/or charge notices.

Non-charging may not affect entitlement or eligibility. The claimant, if eligible and qualified, may still collect benefits. Here are reasons for non-charging and credit:

- Voluntarily quit without good cause connected with the work. Tax rated employer is relieved of all (100%) benefit charges based on the period of employment ending with such separation.

- Discharged for dishonest or criminal act, sabotage or an act endangering safety of others. Must be in connection with work.

- Use of illegal drugs, refusal to take a drug test, or altering a drug test (effective with separations after July 3, 1994) if:

- The employer has a reasonable drug policy.

- The drug test meets Department of Transportation or other reliable standards.

- The employee has been advised of the drug policy in writing.

As application of a disqualification in this category involves removal of base period wages from the claim, reimbursing employers accounts are credited as the claimant repays the benefits for the overpaid weeks the claimant is disqualified.

- Discharged for actual or threatened misconduct in connection with work after previous warning. Tax rated employer is relieved of all (100%) benefit charges.

- Discharged for misconduct connected with work with no warning other than the acts mentioned above. Tax rated employer is relieved of one-half (50%) benefit charges.

- Continues to work part-time with similar wages and hours as those in base period. Tax rated employer is relieved of all (100%) benefit charges.

- If the claimant is originally granted and paid benefits, but as a result of a redetermination or an appeal is later disqualified, a credit will be immediately given—except to reimbursing employers—for benefits paid prior to the redetermination or appeal decision. Credits will only be given to reimbursing employers when the claimant repays any benefits improperly paid. Subsequent benefits will only be charged if the claimant resolves the disqualification and the benefits are otherwise payable.

You may contact the Experience Rating Section if you have questions:

Workforce Alabama

Experience Rating Section

50 North Ripley Street

Montgomery, AL 36130

Phone: 334-954-4741

Fax: 334-242-2068

How do temporary agencies seek relief from benefit charges for school services employees?

Following passage of HB71 , a temporary agency company seeking relief of benefit charges for school services employees must file an affidavit with the Alabama Department of Workforce. Relief of benefit charges will only be considered if 75% or more of the temporary agency’s employees are employed within a school system. To file an affidavit, please click here. For questions concerning your affidavit, call 334-954-4730.

You may mail the notarized original to:

Workforce Alabama

Status Unit

50 N Ripley Street

Montgomery, AL 36130

Quarterly Reports & Wages

How can I get help filling out my Quarterly Contribution and Wage report?

Contact your local field tax representative.

What is the interest rate on past due contributions?

One percent (1%) per month on contributions due until paid.

What is the penalty rate for late reports?

On quarters prior to January 1, 1996, the penalty is $5 per report due. Beginning with first quarter 1996, the penalty is $25 or 10% of taxes owed, whichever is greater.

May I use a computer-generated Contribution and Wage Report?

No. Quarterly reports must be filed online via eGov.

What is the taxable wage base?

The employer is taxed on the first $8,000 paid by the employer to the worker during the calendar year.

May I file one report for the whole year?

No. The Quarterly Contribution and Wage Report must be filed online for each quarter.

How should I make wage corrections?

Submit a completed UC-10-C (Statement to Correct Information) form online via eGov.

How do I obtain a copy of previously submitted Quarterly Contribution and Wage Reports?

For reports filed online, go to eGov and login using the username and password you created.

- Click “Quarterly Reporting/EFT” link, then click “Wage and Tax Reporting (Handkey)” or “Wage and Tax Reporting (upload)” link, whichever is appropriate to your method of filing.

- Enter your UC Account number and Federal identification number and click Submit. Click “Continue” thru the two informational screens.

- From the “Reporting Options” page, click “View/Reset Previously Entered Wage Reports” link, then click on “View Report” link next to the year/quarter report you wish to view and/or print. This will open in a new window. Print the report and exit/close the page.

For other reports, call, write or fax your request to the Audit & Cashiering Section at the address below.

What should I do to correct names or social security numbers already displayed on the online reports?

When filing the report online, check the “delete” box next to the line containing the incorrect name or social security number. Click on “Add New Employee” and input the correct information including name, SSN, etc. To correct previously submitted reports, submit Form UC-10-C online.

Do I have to pay taxes if they are less than $1?

Yes. All taxes due are payable.

When is the last day I can file my Quarterly Contribution and Wage Report and not be late?

Contribution and Wage Reports are due the last day of the month following the end of the quarter (January 31, April 30, July 31, and October 31).

Do I have to pay UC taxes on part-time employees?

Yes.

In sole proprietorships, are spouses and children under 21 exempt from UC taxes?

Yes.

When in Chapter 11 Bankruptcy, am I expected to make quarterly reports and payment of UC taxes?

Yes, you are required to report quarterly and pay post-petition taxes, which accrue following the filing of Chapter 11.

Can our employees participate in a cafeteria plan and receive a reduction in reportable wages?

If the employee has the option of the benefit or receiving cash, it is reportable for Alabama UC purposes.

Are wages paid to an employee by an Alabama employer for employment in another state useable in calculating the $8,000 taxable wages in Alabama?

Yes.

What is the Alabama New-Hire program?

The New-Hire program is a registry for reporting newly hired employees, recalled workers and job refusals. Its purpose is to combat fraud and keep employer tax rates from rising. For more information call the New-Hire Unit at 334-206-6020. You can also learn more from the New Hire page on the Workforce Alabama site.

What information about UC do I need for my employees?

Employers are required to display the posters for Alabama Child Labor Law, Worker’s Compensation Notice and Your Job Insurance.These posters and others can be downloaded from our documents page.

Unemployment Compensation

How do I file a new unemployment claim or re-open an existing claim?

Visit the online claimant portal or call 1-866-234-5382 (select option 2).

How do I file a weekly claim certification?

Visit the online claimant portal or call us:

- Montgomery local area: 334-954-4094

- Birmingham local area: 205-458-2282

- Other areas: 1-800-752-7389.

Who do I contact if I have a specific question or problem with my claim?

Call 1-800-361-4524 after 5 p.m., Sunday through Thursday, to schedule a callback for the next day. If you are unable to secure an appointment, please try again on the next day after 5 p.m. You are only allowed one scheduled callback appointment per week.

Who do I contact to report unemployment tax fraud (being paid cash or receiving a 1099)?

Visit our website at Report Fraud or call 1-855-234-2856.

Who do I contact to report benefit unemployment fraud?

Visit our website at Report Fraud or call 1-800-392-8019.

How do I find general information or frequently asked questions on unemployment compensation?

Check our Unemployment FAQ’s first, particularly the “Claims & Benefits” section, and if you don’t find the answer, check the UC General Inquiry.

What if I have questions about my debit card?

To contact Card Services directly, please call 1-833-888-2779.

What if I have questions about an unemployment compensation overpayment?

Please email ucoverpayments@workforce.alabama.gov or call 334-956-4000.

What if I have questions about Trade Readjustment Allowance (TRA) or Trade Adjustment Assistance (TAA) training programs?

Please call 334-956-7308.

What if I have questions about an employer-filed partial unemployment claim?

Please email partials@workforce.alabama.gov or call 334-956-7481.

How do I request UC-related posters or employer handbooks?

Please call 334-954-3502.

How do I request copies of lost documents or past work history?

Please email disclosureunit@workforce.alabama.gov or call 334-954-4076.

What if I have questions concerning 1099-G forms?

You should receive a Form 1099-G, Certain Government Payments, showing the amount of unemployment compensation paid to you during the year in Box 1, and any federal income tax withheld in Box 4. For more information on unemployment, see Unemployment Benefits in Publication 525.

If you have specific questions about the 1099-G you received, or a missing 1099-G, please email Treasurer@workforce.alabama.gov or call (334) 956-5874.

What if I have questions concerning direct deposit of unemployment compensation benefits?

Please email treasurer@workforce.alabama.gov or call 334-956-5870.

How do I find information regarding unemployment compensation appeals?

Visit the Hearings and Appeals page on our website.

Who do I contact if I am an employer and have questions concerning Employer Tax Account numbers?

Please email status@workforce.alabama.gov or call 334-954-4730.

Who do I contact if I am an employer and have questions concerning delinquent notices, liens or garnishments?

Please email auditcashiering@workforce.alabama.gov or call 334-954-4723.

Who do I contact if I am an employer and have questions concerning experience rating, benefit charging, powers of attorneys or tax rate notices?

Please email experiencerating@workforce.alabama.gov or call 334-954-4741.

Who do I contact if I am an employer and have questions concerning quarterly reports, including copies of past reports?

Please email auditcashiering@workforce.alabama.gov or call 334-954-4701.

Who do I contact if I am an employer and have questions concerning re-certifications of taxable wages or proof of payment (940C)?

Please email auditcashiering@workforce.alabama.gov or call 334-954-4701.

Information Technology

How do I correct the error “Can not load dll msjet” or similar error for the CPUB application I’m trying to use?

Here are the steps to correct this issue:

- From the PC that has Partials (CPUB) installed; Make sure all programs are closed.

- Double click “My Computer” icon from the desktop.

- Double click “C: drive”

- Double click “Program files”

- Double click “AL DIR”

- Double click “jet35sp3”

- A window will open with a message “File progress…transfer file”…. This window will close automatically in a few seconds.

- Now from the desktop, double click the Alabama Department of Labor partials 2.4 icon so the main menu appears.

- Click option number 6 to run initial setup

- A message should appear “The Alabama Department of Labor database has been created”

- The program is ready… click option number 1 to start entering the employee data….

- If you still receive the “Can not load Error”, repeat steps 1 thru 8, then select option number 1.

How do I file New Hire electronically?

Please contact : newhire@workforce.alabama.gov , (334) 206-6020.

Where are the file specifications located for New Hire or Wages?

Please contact : newhire@workforce.alabama.gov , (334) 206-6020.

Please contact : egov@workforce.alabama.gov , (334) 954-4701.

How do I get my format approved for filing of New Hire or Wages?

Please contact : newhire@workforce.alabama.gov , (334) 206-6020.

Please contact : egov@workforce.alabama.gov , (334) 954-4701.

Do I have to change the format of wages I am currently using to file the Egov method?

Please contact : egov@workforce.alabama.gov , (334) 954-4701.

If I am locked out of my Egov account and need assistance?

Please contact : egov@workforce.alabama.gov , (334) 954-4701.

Can someone assist me while I am filing the Egov method?

Please contact : egov@workforce.alabama.gov , (334) 954-4701.

If you have questions about filing UC-CR4 electronically …

Please contact : the Audit and Cashiering Unit at (334) 954-4701 or auditcashiering@workforce.alabama.gov.

If you have questions about registering for an unemployment compensation account number …

Please contact the Status Unit at (334) 954-4730 or status@workforce.alabama.gov.

If you have questions about resetting eGov login and/or password …

Please contact the Audit and Cashiering Unit at (334) 954-4701 or auditcashiering@workforce.alabama.gov.